Optimise

your Trust.

Feel like you're paying

too much tax

on your Trust?

You might be right.

Trusts are a common business structure, and they have their pros and cons in terms of strategy and practicality. If you have a profitable business, you operate from a Trust, but you don’t know what a bucket company (aka corporate beneficiary) is, then you could be missing out on some of the benefits of a Trust structure and paying too much tax in the process.

The ultimate objective of any good tax planning strategy is minimising the average tax rate of your family group AND deferring the due date of tax payable on income. A bucket company can help with both of these.

For the 2020 financial year, the top individual tax rate is 47%, while a bucket company pays tax at 30%, so you can see where we’re going here. High income earns also pay more tax on their super contributions, and if they don’t have private hospital cover, pay a Medicare Levy Surcharge.

Who can use

this strategy?

A bucket company structure could be suitable for;

- Business owners or investors

- Who run their business in a Trust or receive investment income in a Trust, and

- Who are not caught by the Personal Services Income (PSI) rules

A bucket company structure works really well where;

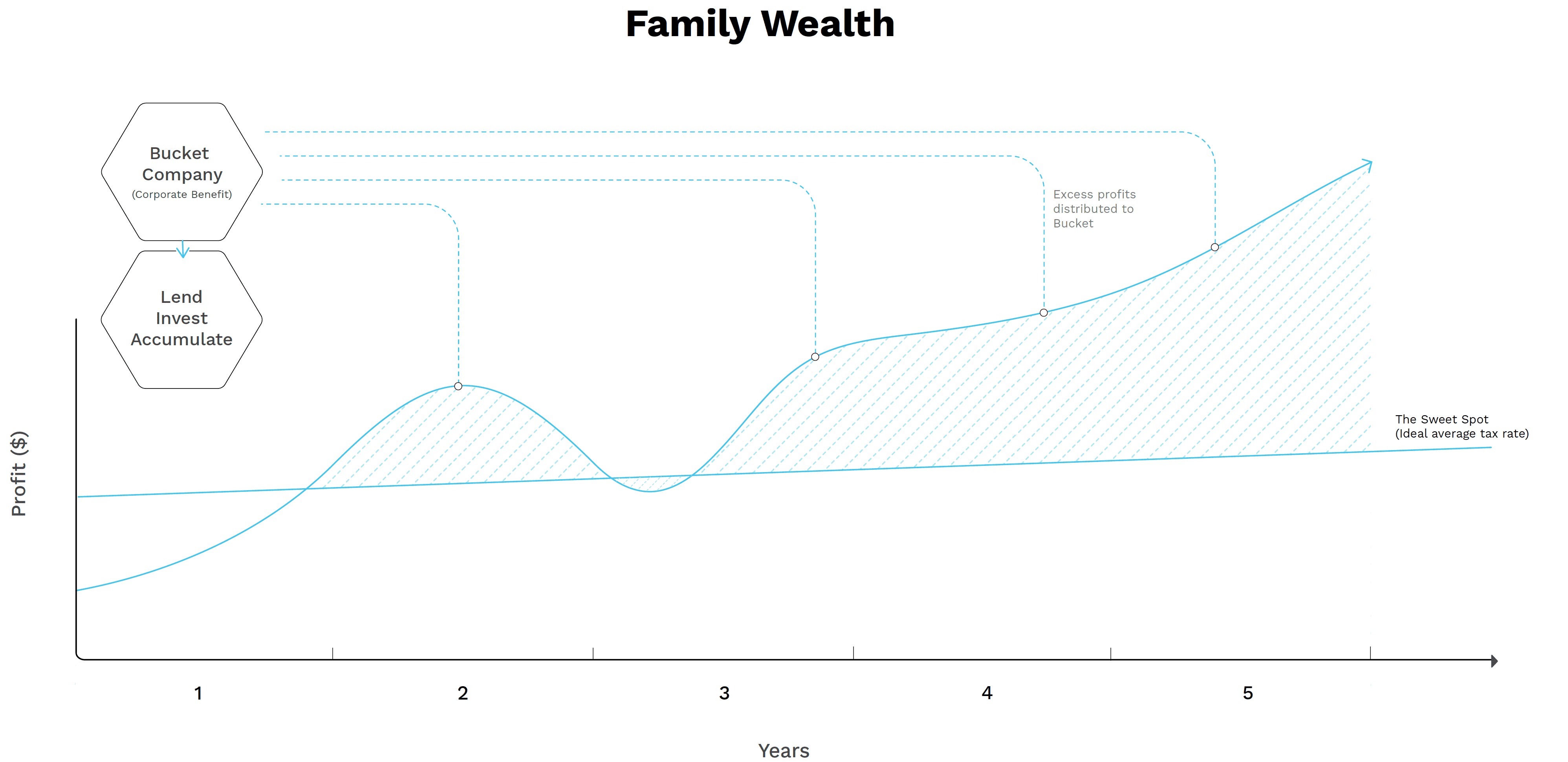

- A business has surplus income available to its owners above their cost of living, and they want to build wealth in their family group to use for business and investment purposes

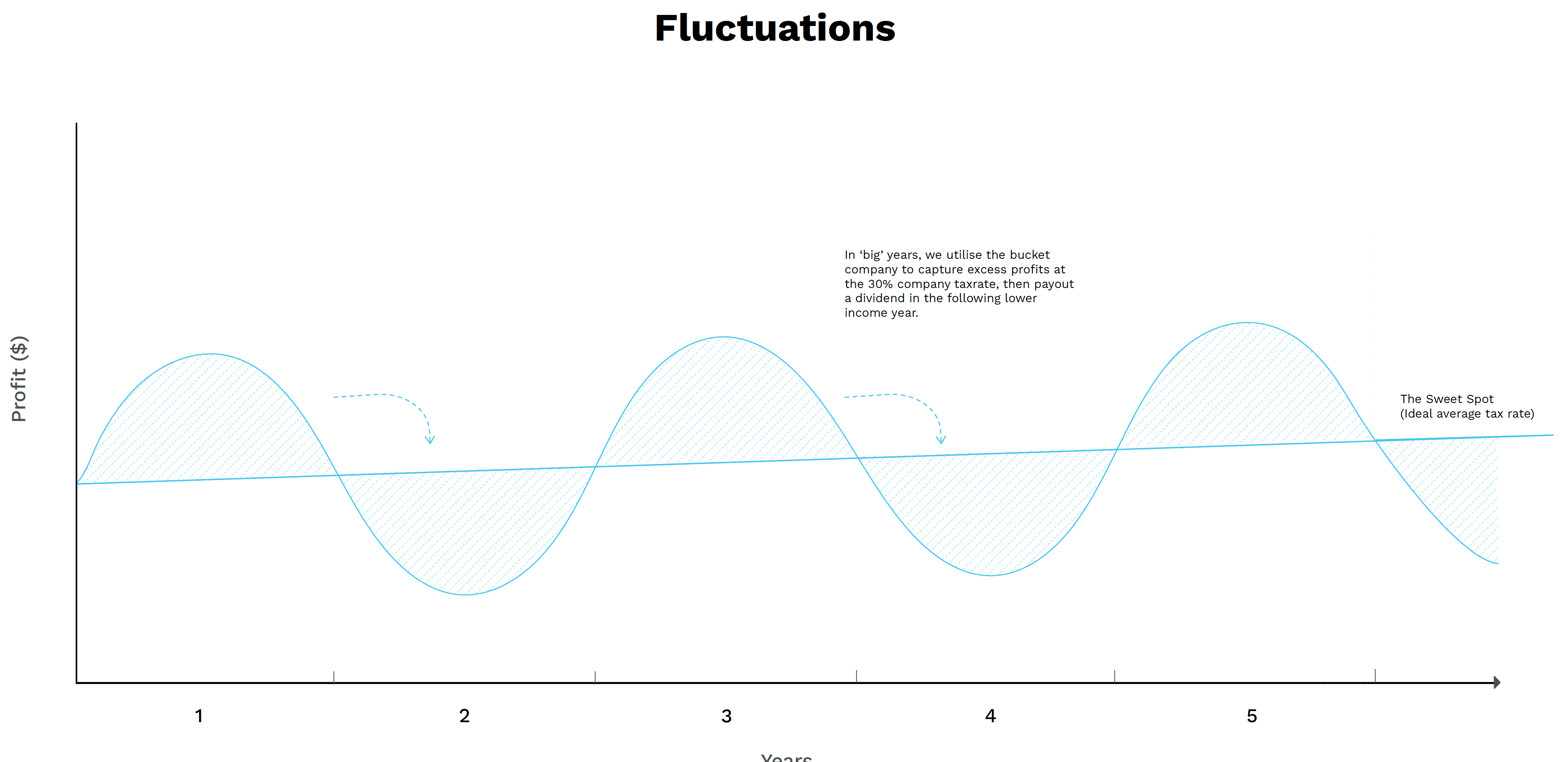

- The profits of a business fluctuate significantly from year to year and it makes sense to defer tax on profits in ‘big’ years

- Business owners are getting ready for retirement, and plan on want to maximise their after tax income during retirement.

***Diagram 1 basically applies here too, except the bucket will pay them a dividend each year as a supplementary income stream**

In the right circumstances, a family group with a property managed bucket company can save many thousands of dollars in tax each year.

How it

works.

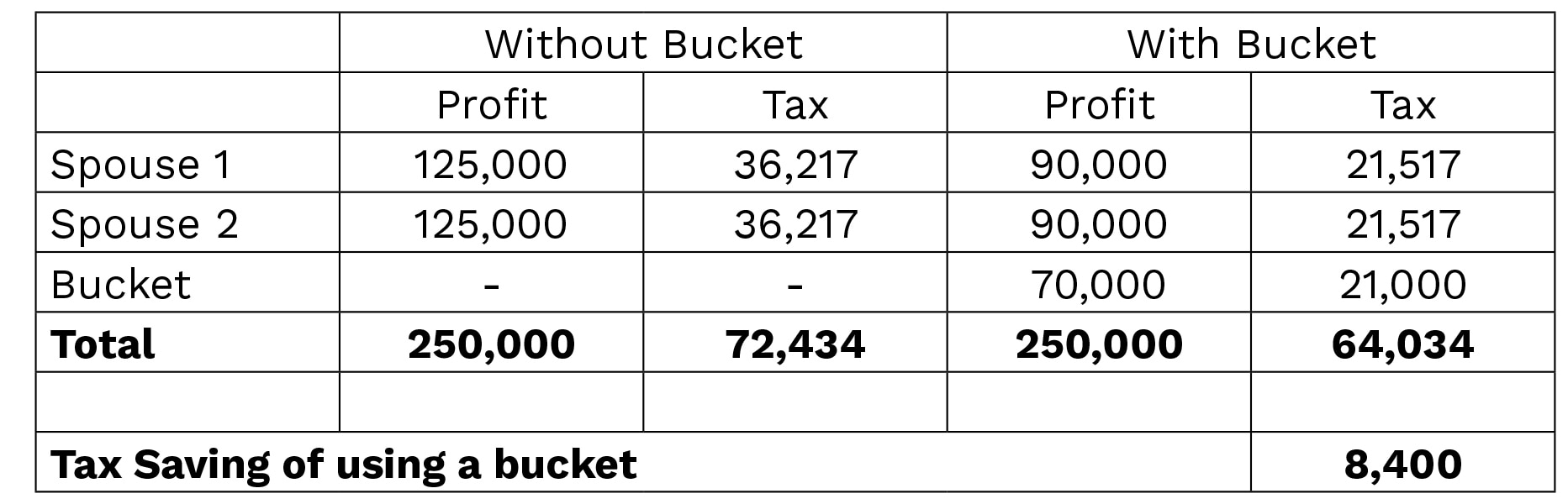

Lets say you run a business which generates a profit of $250k for the year. This needs to be distributed to beneficiaries (individuals or entities) come tax time. It’s the beneficiaries of the Trust who pay the tax on income.

Looking at the basic scenario below, you can see that there is a significant tax saving which can be achieved through the use of a bucket company to take excess profit.

We’ve used $90k as the sweet spot for the spouse income since a combined family income of 180k is a decent amount to cover living expenses and it means you avoid paying the higher rates of tax in your own name (39% and 47%).

What's

the catch?

There is no ‘catch’ but the strategy needs to be done properly and the money needs to follow the distributions on paper.

Good tax planning is achieving the lowest possible average tax rate each year and deferring tax payments until some time in the future. Bad tax planning is spending money on things you don’t need to reduce your business profit.

If the business above was a cyclical business, and the year in question was a ‘big’ year, the company might pay a dividend back to the individuals in a ‘quiet’ year, thus helping to smooth out the tax rates and achieve the objective of the lowest possible average tax rate and deferring tax payments until the future.

Other

interesting points.

- A properly managed bucket company can act as your family ‘bank’. Lending accumulated cash out to business and investment entities at an ATO sanctioned rate (5.37% in 2020) for up to 7 years (unsecured) and up to 30 years (unsecured). This way you can avoid dealing with banks for some or all of your funding requirements – great when you need to access funds for a deposit on a property.

- You can invest the funds in the bucket company directly, but its important to note that there is no Capital Gains Tax (CGT) discount available to a company and so this should be considered when choosing investments for the company.

- Its important to consider who owns the bucket company. Ideally, the bucket company will be owned by a separate investment Trust. This gives ultimate flexibility as to who receives the dividends from the Trust AND provides the greatest level of asset protection. Bucket companies should never be owned by individuals.

- If you are using a bucket company strategy and are planning to retire soon, think of it as another super fund. Lets say your are receiving a tax free pension from your super fund, and have minimal other income in your own name, now is the time to start paying yourself a dividend from the bucket company. You pay not tax on the first $18,200 of income and only 21% on income up to $37k. This means that you can receive dividends in retirement AND get the benefit of the tax already paid by the company on those profits years earlier.

Key takeway

This is a high level summary of the operation of a bucket company as part of a family group with a Trust running a business (or managing an investment portfolio). The key takeaway for everyone with a Trust is that you should be aware of if and how it is being used to help you achieve the best possible tax result. If you are unsure of how your group is structured, or you want a second opinion on your situation.

4 simple steps to reduce your tax:

We want to get to know you and your business and we know you want to get to know our accountants. So, we hold a relaxed, informative consultation that allows just that. Over a cup of great coffee, we can talk about your goals, and develop a strategy, while you get to see how we work.

Let's connect

We've been waiting to hear from you!